Zero Cost Credit Card Processing: Smart Strategy or Costly Mistake?

Zero cost processing strategies such as surcharging and cash discount programs can reduce processing costs, but they are not right for every business. CPP helps merchants evaluate customer impact, compliance requirements, workflow considerations, and alternatives before implementation.

Zero Cost Processing Isn't Free Processing

The name sounds simple. The strategy is not. Zero cost processing usually shifts card acceptance costs from the business to the customer through a surcharge, cash discount, or service fee program.

The better question is not whether you can reduce fees. The better question is whether doing so improves profitability without creating customer friction.

Surcharge Programs

Add a fee when customers pay by credit card.

Cash Discount Programs

Offer customers a lower price when they pay with cash.

Service Fee Programs

Used in specific payment environments with strict rules.

Not Sure Which Model You’re Actually Comparing?

Surcharges, cash discounts, and dual pricing are often grouped together, but they create different compliance, pricing, and customer experience considerations.

Read our guide: Surcharge vs Cash Discount vs Dual Pricing: What’s the Difference?

When Zero Cost Processing Makes Sense

Zero cost programs often work best when payment convenience matters more than the fee itself.

B2B Companies

Invoice-based payments where speed, convenience, and card acceptance matter.

Professional Services

Law firms, consultants, medical offices, and service providers with higher-value transactions.

High-Ticket Sales

Businesses where payment flexibility can outweigh surcharge sensitivity.

When Zero Cost Processing Creates Challenges

A surcharge can reduce processing costs while quietly hurting revenue, reviews, referrals, or checkout completion.

Customer Pushback

Some customers see added fees as a penalty, not a payment option.

Lower Conversion

Online checkout pages and invoice payment links can take a hit.

Staff Confusion

If the program is not explained clearly, front-line teams create risk.

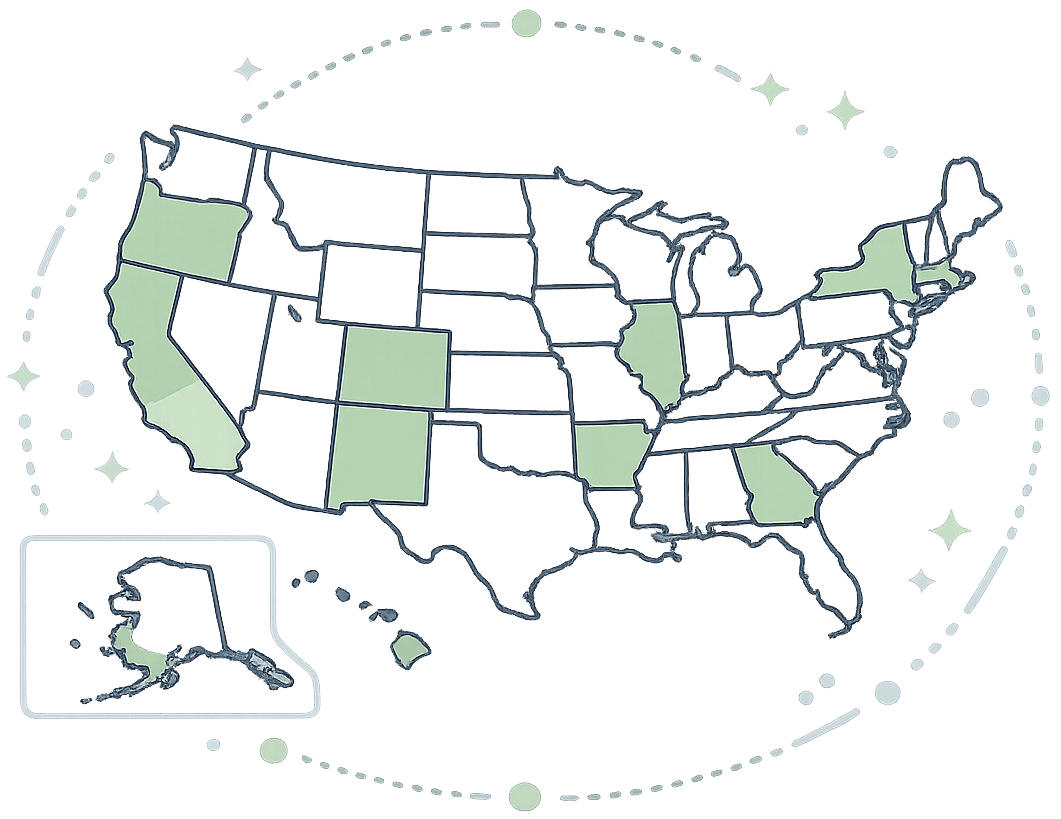

Surcharge Rules Vary by State and Card Brand

Surcharging may involve state rules, card brand registration requirements, receipt disclosures, debit card restrictions, fee caps, and customer notification obligations.

Why Compliance Should Be Evaluated Early

Regulations and card brand requirements can change. Before implementing any surcharge or cash discount program, businesses should understand how those rules apply to their specific payment environment.

CPP helps merchants evaluate compliance requirements alongside customer experience, workflow design, and profitability considerations before recommending a program.

Credit Card Surcharge Laws by State ()

State rules, disclosure requirements, and implementation considerations can vary. Before launching a surcharge program, understand how current regulations may apply to your business.

View State-by-State Guide →Where Payment Costs Really Come From

Many businesses can reduce processing costs by fixing payment workflows, qualification issues, verification settings, recurring billing strategies, and invoice processes without adding fees to customer transactions.

Interchange Qualification

Identify transactions that are downgrading unnecessarily and increasing processing costs.

Invoice Workflows

Improve how customers receive, access, and pay invoices to increase efficiency and reduce friction.

AVS Settings

Reduce avoidable qualification issues and unnecessary declines caused by verification settings.

Virtual Terminal Use

Optimize manually entered transactions and card-not-present workflows.

Recurring Billing

Improve stored payment methods, subscription workflows, and repeat payment performance.

Gateway Configuration

Review how payment tools, hosted payment pages, terminals, and integrations are configured.

How We Determine Whether Surcharging Makes Sense

A processor sells a program. CPP evaluates the strategy first.

The goal is not simply to reduce processing costs. The goal is to improve profitability, maintain customer satisfaction, and eliminate avoidable payment inefficiencies.

Sometimes the answer is a surcharge program. Sometimes it's workflow optimization. Sometimes it's both.

Review Current Processing

We examine statements, fees, transaction types, and payment channels.

Analyze Customer Experience

We identify where customer friction may occur and how payment behavior could change.

Evaluate Compliance

We review applicable state requirements, card brand rules, and disclosure obligations.

Find Alternative Savings

We identify optimization opportunities that may reduce costs without adding customer fees.

Recommend the Best Path

Surcharge program, cash discount, workflow optimization, or no change at all.

Common Questions About Zero Cost Processing

What is zero cost processing?

Zero cost processing is a payment strategy that shifts some or all credit card acceptance costs from the business to the customer through a surcharge, cash discount, or service fee structure.

Is zero cost credit card processing legal?

It depends on the program structure, state requirements, card brand rules, and how fees are disclosed to customers.

What is the difference between a surcharge and a cash discount?

A surcharge adds a fee when a customer pays by credit card. A cash discount reduces the price when a customer pays by cash or another qualifying payment method.

Can I surcharge debit cards?

Debit card surcharging is generally prohibited, including many transactions processed without a PIN. For a deeper explanation, read: Can You Surcharge Debit Cards? The Answer Most Businesses Get Wrong .

How much can a business surcharge customers?

Surcharge limits are governed by card brand requirements and other regulations. Businesses should review current requirements before implementation.

Can online payments be surcharged?

In many situations, yes. However, disclosure requirements, checkout presentation, and card brand rules must be followed carefully.

Can invoice payments be surcharged?

Invoice-based businesses often implement surcharge programs successfully, but customer experience and compliance considerations should be reviewed first.

Can recurring payments be surcharged?

Some recurring billing environments can support surcharge programs, but implementation requirements vary based on payment method and workflow.

What states allow credit card surcharges?

Surcharge rules vary by state and may change over time. Businesses should verify current requirements before implementing a program.

Will customers complain about surcharges?

Some customers will. The impact depends on your industry, competition, average ticket size, and how the program is communicated.

Can I reduce processing costs without surcharging?

Often, yes. Payment workflows, qualification settings, recurring billing, invoicing, and verification rules can all affect processing costs.

Do I need special equipment for a surcharge program?

Not always. Requirements vary based on whether payments are accepted in person, online, through invoices, or through recurring billing systems.

How do I know if surcharging is right for my business?

The answer depends on your customers, industry, payment channels, competitive environment, and current payment workflow. That evaluation should happen before implementation.

Before You Add Fees to Customer Transactions, Know Your Options

CPP helps businesses evaluate surcharge programs, cash discount programs, compliance requirements, customer experience, and hidden savings opportunities that may reduce costs without changing the way customers pay.