Surcharge Disclosure Requirements

Credit Card Surcharge Disclosure Requirements: Signs, Receipts, and Customer Notifications

Credit card surcharge disclosure requirements are often one of the most important parts of a successful surcharge program. Customers should understand what they are paying, why they are paying it, and when the fee applies.

Credit card surcharge disclosure requirements are often one of the most overlooked parts of implementing a surcharge program. Many business owners assume that adding a surcharge is mostly about turning on a fee.

In reality, disclosure requirements are often one of the most important parts of a successful surcharge program.

Card brands, state requirements, payment platforms, and customer expectations all influence how surcharge disclosures should be presented.

Unfortunately, many surcharge problems occur because merchants focus exclusively on the fee itself while overlooking customer communication.

A surcharge program can be technically compliant and still create customer complaints, negative reviews, abandoned checkouts, billing disputes, and staff confusion if disclosures are handled poorly.

That is why businesses evaluating surcharge programs should focus on two separate goals: compliance and customer experience. Both matter.

If you are still evaluating whether surcharging is the right approach, review our guide to Surcharge vs Cash Discount vs Dual Pricing: What's the Difference? before making implementation decisions.

What Are Credit Card Surcharge Disclosure Requirements?

Credit card surcharge disclosure requirements generally refer to the notices, signage, communications, and transaction-level disclosures used to inform customers that a surcharge may apply when paying by credit card.

Requirements may vary based on:

- State-specific regulations

- Card brand requirements

- Payment channel

- Processor requirements

- Gateway capabilities

- Business model

Rules may change over time, so businesses should verify current requirements before implementation.

While exact requirements vary, surcharge disclosures commonly involve:

- Point-of-sale signage

- Checkout notices

- Receipt disclosures

- Invoice payment disclosures

- Online payment page disclosures

- Recurring billing disclosures

- Customer notifications

- Employee communication procedures

The goal is transparency.

Customers should not discover a surcharge only after completing payment.

Why Surcharge Disclosure Matters Beyond Compliance

Many competing articles discuss disclosure requirements as a legal checklist.

That approach misses a larger business reality.

Most customers do not care whether your surcharge program technically satisfies a card brand rule.

They care whether the charge feels transparent and fair.

Business A posts a small sign near the register and applies a fee without explaining it.

Business B explains the fee clearly on invoices, payment pages, receipts, customer communications, and staff conversations.

Both may technically comply. Only one creates a better customer experience.

This distinction becomes even more important for medical practices, dental offices, law firms, professional service firms, recurring billing businesses, and invoice-driven businesses.

These organizations often rely on long-term customer relationships where trust matters more than a single transaction.

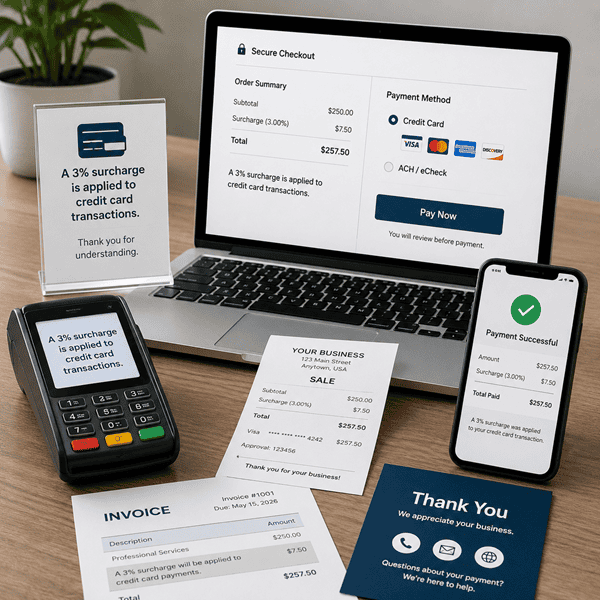

Point-of-Sale Surcharge Signage Requirements

For in-person payments, signage is often one of the first disclosure elements customers encounter.

Signs should be easy to locate and easy to understand.

Businesses frequently place surcharge notices:

- Near entrances

- At reception desks

- At checkout counters

- Near payment terminals

The purpose is to notify customers before payment occurs.

Poor signage creates problems when customers only discover the fee after inserting or tapping their card.

Even if a surcharge program is otherwise compliant, poor sign placement can create unnecessary frustration.

Good signage should prioritize visibility and clarity rather than legal complexity.

Credit Card Surcharge Receipt Requirements

Receipts are another important component of surcharge transparency.

Customers should be able to see:

- Transaction amount

- Surcharge amount

- Total amount charged

Receipt presentation matters.

A surcharge hidden inside a generic line item may create confusion.

A clearly identified surcharge is easier for customers to understand and easier for staff to explain.

Businesses should periodically test receipts to verify:

- Fee calculations

- Tax treatment

- Payment totals

- Display formatting

- Credit versus debit handling

This becomes especially important when multiple payment channels are involved.

Online Credit Card Surcharge Disclosure Requirements

Online payments introduce additional disclosure challenges.

Customers cannot ask a cashier questions.

The payment page must communicate clearly on its own.

Before Payment Entry

Customers should understand that a surcharge may apply before entering payment information.

During Checkout

The surcharge should be presented clearly near the total transaction amount.

Confirmation Screens

Customers should be able to confirm the total before submitting payment.

Payment Receipts

Receipts should clearly show the surcharge amount and total amount charged.

Poorly implemented disclosures can increase cart abandonment, customer complaints, payment disputes, and support requests.

For businesses processing substantial online volume, checkout transparency directly affects conversion performance.

This is one reason CPP evaluates surcharge programs as payment optimization projects rather than simple fee programs.

Invoice Payment Link Disclosures

Many businesses collect payments through emailed invoices and hosted payment pages.

Invoice-based environments create unique disclosure considerations because customers often pay days or weeks after receiving the original invoice.

Disclosure opportunities may include:

- Invoice language

- Email payment requests

- Hosted payment pages

- Payment selection screens

- Final payment confirmations

The customer should understand applicable fees before completing the transaction.

Businesses that rely heavily on invoice payments should also evaluate whether ACH adoption could reduce costs without introducing customer-facing fees.

For many organizations, zero cost credit card processing strategies should be evaluated alongside ACH opportunities rather than in isolation.

Email Payment Request Disclosures

Email payment requests deserve special attention.

Many merchants send payment links with little explanation.

Customers then arrive at a payment page and encounter an unexpected surcharge.

This creates avoidable friction.

A simple explanation inside the payment request email can often improve transparency and reduce support inquiries.

When evaluating surcharge communications, businesses should review the entire payment journey rather than focusing on a single screen.

Recurring Billing Surcharge Disclosure Requirements

Recurring billing environments require additional planning.

Customers are not present for every transaction.

That makes communication especially important.

Businesses should evaluate:

- Initial customer agreements

- Stored payment authorizations

- Billing notifications

- Customer acknowledgments

- Ongoing communication procedures

Recurring billing disclosures should clearly explain when fees apply and how they are calculated.

Requirements vary depending on the payment environment, so compliance review is recommended.

Recurring billing programs that are configured incorrectly can create customer dissatisfaction that persists for months before being discovered.

Debit Card Handling and Surcharge Disclosure Risks

One of the most common surcharge mistakes involves debit cards.

Many businesses assume a surcharge can be applied to all card transactions.

That assumption creates risk.

Debit card restrictions remain one of the most important surcharge compliance considerations.

If you are unfamiliar with these rules, review Can You Surcharge Debit Cards? The Answer Most Businesses Get Wrong.

Businesses should verify that:

- Debit cards are identified correctly

- Debit transactions are excluded when required

- Receipts display properly

- Payment systems process fees appropriately

Disclosure alone does not solve improper debit card handling.

The underlying payment workflow must also be configured correctly.

Customer Communication Matters More Than Most Businesses Realize

Many merchants underestimate how strongly communication affects customer perception.

The fee itself may not generate complaints.

The surprise often does.

Website FAQs

Help customers understand payment options before they reach checkout.

Invoice Language

Prepare customers before they click a payment link.

Payment Page Messaging

Explain applicable fees before payment is submitted.

Staff Explanations

Make sure customer-facing employees can explain the program clearly.

The objective is not simply to disclose the fee.

The objective is to eliminate confusion.

Businesses with strong customer communication often experience fewer disputes, fewer complaints, and smoother implementation.

Staff Training and Internal Communication

Staff members frequently become the face of the surcharge program.

Customers ask questions.

Employees provide answers.

Without training, confusion spreads quickly.

Employees should understand:

- When fees apply

- When fees do not apply

- Debit card restrictions

- Customer explanation procedures

- Escalation processes

A well-trained staff can improve customer acceptance significantly.

A poorly trained staff can undermine even a technically compliant program.

State-Specific Surcharge Disclosure Considerations

Disclosure requirements can vary depending on location.

Some states place greater emphasis on pricing transparency.

Others may impose specific disclosure requirements.

Because laws and interpretations change, businesses should review current requirements before implementation.

Our guide to Credit Card Surcharge Laws by State: What Merchants Need to Know provides additional information about state-level surcharge considerations.

Businesses operating across multiple states should pay particular attention to consistency and compliance review.

What Happens When Surcharge Disclosures Are Missing?

Missing disclosures can create several problems.

Customer Complaints

Customers are more likely to complain when fees feel unexpected.

Payment Disputes

Confusing surcharge presentation can increase billing questions and disputes.

Negative Reviews

Poor communication can turn a payment fee into a reputation issue.

Operational Confusion

Staff may struggle to explain the program when disclosures are inconsistent.

Even when enforcement is not involved, poor disclosure practices can damage customer trust.

Most businesses implement surcharge programs to improve profitability.

Poor communication can undermine that goal.

Disclosure Quality Can Make or Break the Program

Successful surcharge programs require more than fee activation. Customers need clear communication before payment, during payment, and after payment.

When disclosures are unclear, the surcharge becomes the story. When disclosures are clear, the payment option is easier for customers to understand.

Surcharge disclosures should be reviewed across signs, receipts, invoices, hosted payment pages, online checkout, and recurring billing workflows.

What CPP Reviews Before Recommending a Surcharge Program

Most providers focus on whether a surcharge can be implemented.

CPP focuses on whether it should be implemented and how it will affect the overall payment environment.

Before recommending a surcharge strategy, CPP reviews:

- Customer communication practices

- Invoice workflows

- Online checkout flows

- Hosted payment pages

- Gateway configuration

- Debit card handling

- Receipt presentation

- Staff training procedures

- Recurring billing workflows

- Compliance considerations

- ACH adoption opportunities

- Customer payment behavior

- Average transaction size

This review often identifies opportunities that have little to do with surcharging.

In many cases, workflow improvements, AVS optimization, gateway configuration changes, recurring billing improvements, or ACH adoption may reduce costs without introducing customer-facing fees.

That broader perspective is what separates payment optimization from simple fee implementation.

Related Resources

If you're evaluating surcharge disclosure requirements, these resources can help you understand state rules, debit card restrictions, pricing models, and payment optimization alternatives.

Compliance Reminder

Rules vary. Requirements may change over time. Compliance review is recommended before implementation. No article can replace current legal or compliance guidance.

For current card brand requirements, merchants should review Visa surcharge guidance.

Conclusion

Credit card surcharge disclosure requirements involve much more than posting a sign.

Businesses should think about the entire customer payment experience, including receipts, invoices, online payments, recurring billing workflows, debit card handling, employee communication, and customer expectations.

Compliance matters.

Customer experience matters too.

The strongest surcharge programs combine both.

When disclosure practices are clear and workflows are properly configured, businesses can reduce confusion, improve transparency, and create a better payment experience for customers.

The $500 Challenge

Considering a Surcharge Program?

Before adding fees to customer transactions, make sure your disclosures, workflows, payment channels, customer communications, and compliance procedures are working together.

CPP helps businesses evaluate surcharge programs, customer experience impact, debit card handling, online payment workflows, recurring billing considerations, and alternative cost-reduction opportunities.

Take the $500 Challenge and see whether hidden payment inefficiencies are costing your business more than you realize.

Take the $500 ChallengeFAQ

Do I need to post signs for a surcharge program?

In many cases, signage is an important part of surcharge disclosure. Requirements vary, so businesses should verify current rules and card brand requirements before implementation.

Do surcharge disclosures need to appear on receipts?

Receipt disclosure is commonly used to show the surcharge amount and total transaction amount. Clear receipt presentation improves transparency and customer understanding.

Do online surcharge programs require disclosures?

Yes. Online payment environments typically require customers to be informed before completing payment. Businesses should review checkout disclosures carefully.

Can invoice payments be surcharged?

Many invoice-based businesses implement surcharge programs successfully. However, disclosures, payment links, customer communication, and workflow design should be reviewed.

How should recurring billing surcharges be disclosed?

Recurring billing programs generally require clear customer communication regarding fees, payment authorization, and billing practices. Requirements vary by payment environment.

What happens if surcharge disclosures are missing?

Missing disclosures may lead to customer complaints, disputes, operational confusion, compliance concerns, and negative customer experiences.

Do disclosure rules vary by state?

Yes. State-specific requirements can vary and may change over time. Businesses should verify current requirements before implementation.

Can customers dispute surcharge fees?

Customers may dispute charges for many reasons, including confusion about fees. Clear disclosures and communication can help reduce misunderstandings.